The Fed’s triple mandate and recent rating changes in the euro area

The Fed is traditionally defined as having a dual mandate: controlling inflation and unemployment. Its counterparts, such as the European Central Bank, focus primarily on keeping inflation in check. Lately, however, attention has turned to the Federal Reserve Reform Act of 1977—the most recent congressional directive—which established a third mandate: maintaining moderate long-term interest rates, typically measured by the 10-year yield (although it can be argued that this is a natural consequence of keeping inflation under control).

Exact wording of the Federal Reserve Reform Act of 1977:

“The Board […] shall maintain long run growth of the monetary and credit aggregates commensurate with the economy’s long run potential to increase production, so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.”

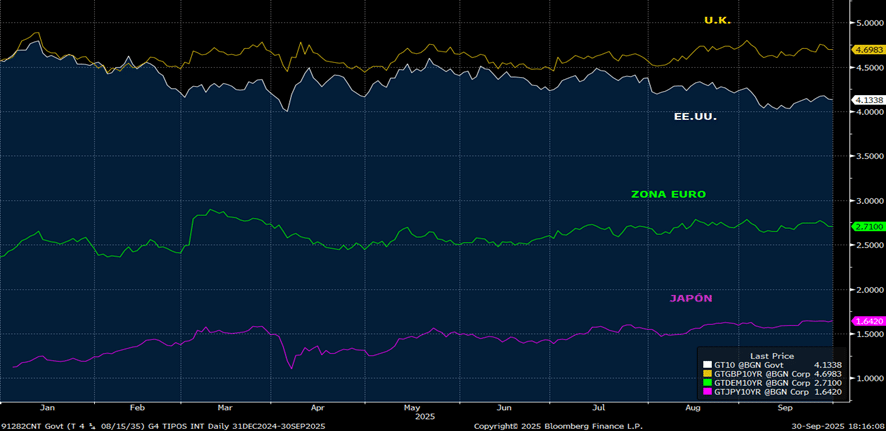

Looking at the 10-year government bond yield curves of the G4 (US, UK, euro area and Japan), these are the only ones that have managed to keep yields below where they started the year. This has been remarkably effective, allowing them to contain borrowing costs at more moderate levels. The pressure for short-term rates to come down will only reinforce this trend, helping governments secure financing at lower levels in the near term as well.

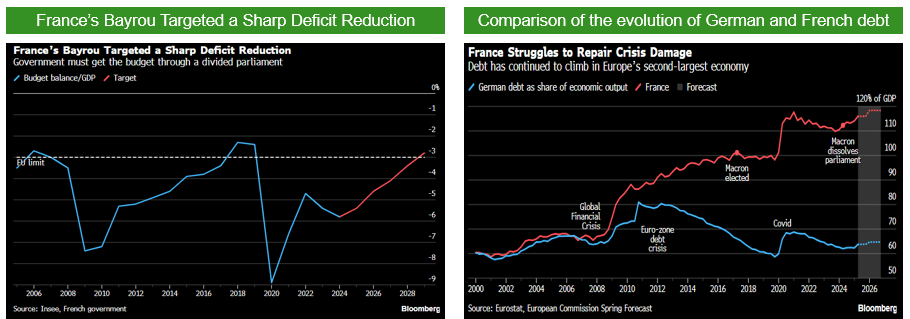

Recent political developments have reignited uncertainty about the fiscal debt burden, with rating agencies particularly active in the euro area—upgrading Spain, Italy and Portugal, while Fitch downgraded France.

Fitch, Moody’s and S&P raised Spain’s rating, acknowledging the country’s resilience. S&P highlights a decade of private-sector deleveraging that has improved the external balance, as well as strong growth prospects above the European average, supported by population growth (immigration), rising employment and robust domestic demand (forecasting GDP growth of +2.6% in 2025). It also notes Spain’s limited exposure to US tariffs. On the other hand, S&P warns that “political deadlock constrains policy impetus. No budget has been passed since 2023, leaving fiscal adjustment modest despite strong economic growth.”

Fitch upgraded PORTUGAL’s rating from ‘A–’ to ‘A’ with a stable outlook, underlining fiscal consolidation, a sharp reduction in debt and improvements in external metrics. Fitch noted that public debt fell from 134.1% of GDP in 2020 to 96.4% in the first quarter of 2025, while public finances remain solid with a projected surplus in 2025 (+0.1% of GDP) and small deficits in 2026–2027. On the external side, Portugal continues a steady process of deleveraging, while the economy has shown resilience. Fitch forecasts GDP growth of 1.8% in 2025 and 2.2% in 2026—above the euro area average—driven by consumption, tax cuts, and a lower interest rate environment, before slowing to 1.7% in 2027.

Fitch upgrades ITALY’s rating to ‘BBB+’ with a stable outlook. The agency highlighted the country’s greater fiscal resilience. Fitch expects a continued gradual deficit reduction in 2025-2027, supported by structural improvements on the revenue side and strict expenditure control. It forecasts a deficit of 3.1% of GDP this year (versus the 3.3% official target). The authorities remain committed to spending restraint, aiming to bring down the deficit to 2.6% in 2027 and under 2% by 2029. Italy’s debt fell by over 20 percentage points in 2020-2024. Debt will remain much higher than peers (the ‘BBB’ median was 57.3% in 2024), but reduced risks can be seen in terms of debt financing and sustainability.

Fitch downgraded France’s long-term rating from ‘AA–’ to ‘A+’. The outlook remains stable. This decision reflects the following drivers: 1) High and rising debt ratio: France’s debt ratio for 2024 is now the third highest among countries in the ‘A’ and ‘AA’ rating categories. 2) Political fragmentation hinders consolidation: Fitch believes that it is unlikely that the deficit will be brought down to 3% by 2029. This includes a weak record of fiscal consolidation and compliance with EU fiscal rules. Fitch was the first credit rating agency to downgrade France within the ‘A’ category, and there is little doubt that other agencies will follow suit in the short to medium term for the same reasons cited by Fitch—unless the country achieves a major political agreement that delivers clear and credible fiscal plans. Failing this, French public debt is expected to rise, with forecasts pointing to an increase of 10 percentage points by 2030, taking it to above 120%. The country’s public debt will remain elevated and is far from the stabilisation threshold (5.5% projected for 2025 compared to the 2.8% required to stabilise the public debt level).

Date of report: October 6th 2025