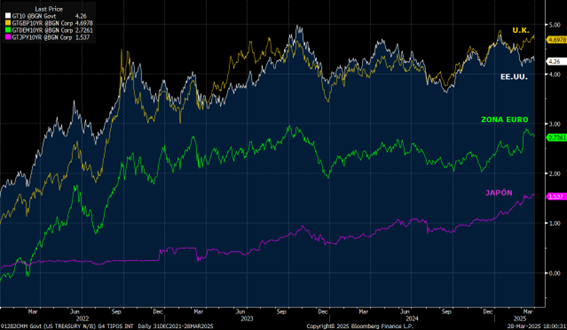

Central banks continue to move at differing paces as they approach their respective terminal rates. At its meeting on 19 March 2025, the Federal Reserve held the federal fund rate steady at 4.25–4.50%. The updated dot plot—the projection of interest rate expectations by FOMC members—indicated that the median forecast still anticipates two rate cuts in 2025, while markets are currently pricing in up to three. The Fed revised its 2025 core inflation forecast upwards by 0.3%, while growth expectations were downgraded by 0.4%, signalling a tilt towards a more stagflationary outlook. Powell said that monetary policy is in a “good place” and emphasised that there is no rush to cut rates.

At its latest meeting on 6 March 2025, the ECB cut its key interest rate by 0.25 basis points, bringing the deposit rate to 2.50%. This marks a cumulative easing of 150 basis points to date. Elevated defence spending and persistent inflation may prevent these rates from falling below the 2% level previously projected (the markets still expect two further cuts this year), and the ECB may opt to pause amid ongoing geopolitical tensions and economic policy uncertainty (namely, the trade tariffs). As a result, the ECB has refrained from committing to a predefined path for interest rates.

Looking at interest rate trends, of particular note was the rise in German Bund yields in the first week of March, with a surge of 43 basis points—the largest weekly increase since German reunification in 1990. This was driven by announcements from the EU regarding plans to boost defence investment by €800 billion, alongside proposals from Germany for a constitutional reform aimed at markedly increasing public spending, particularly in defence and infrastructure. In contrast, 10-year Treasury yields declined, reflecting concerns over a potential slowdown in the US, reinforced by disappointing consumer confidence data.

(G4 government bond yields)

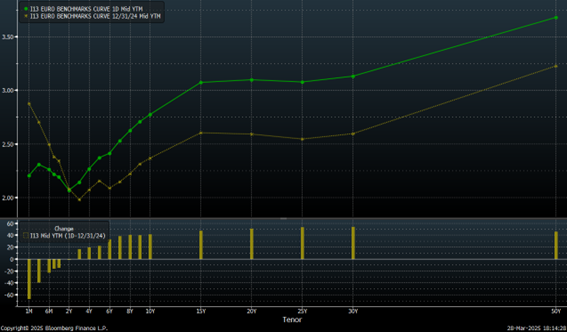

The steepening of the yield curve continues to gather pace. Expectations of further rate cuts by the ECB, combined with anticipated higher sovereign issuance to finance the EU’s defence plans and increased spending in Germany have boosted long-term yields.

(Comparison of the EUR benchmark yield curve between 31/12/2024 and 28/03/2025)

Credit spreads have remained resilient, even in the face of a notable rise in interest rates. We maintain a preference for euro-denominated investment grade credit over its US dollar counterpart, supported by a favourable environment of steady inflows, generally solid fundamentals and a contained default rate. Expansionary fiscal policy and any de-escalation in the war in Ukraine could serve as a catalyst, and Germany would be particularly well positioned to benefit. We continue to see value in the financial sector, and cyclical sectors are likely to outperform more interest rate-sensitive sectors such as utilities and telecommunications.

(iTraxx Main (IG) and Xover (HY) spread trends)

In summary, the easing cycle is nearing its end, although we still anticipate some further rate cuts. The yield curve is steepening, indicating the re-emergence of a term premium—supporting an extension of portfolio duration as yields pick up. At the same time, the spread between corporate and government bond yields has been narrowing (currently at +36 basis points, based on the main European Bloomberg indices), prompting greater interest in sovereign bonds, supranational entities and government agencies among investors assessing the risk-return-liquidity trade-off.

Date of report: March 31st 2025