For Brazil’s financial markets, 2024 has been an exceptionally challenging year. For one, the Brazilian real reached its lowest level in history against the US dollar in December, depreciating by 27.35% over the period. Moreover, government-issued bonds saw a sharp rise in yields, surpassing 15%—levels not seen since 2016.

How did we get here? At other points in history, external factors such as the strength of the US dollar has played a significant role in the poor performance of Brazilian assets. While the recent robustness of the greenback cannot be entirely dismissed, this time, the focus must turn to domestic factors within the country.

The primary concern for the market is fiscal deterioration. Brazil’s deficit exceeded 9% in September 2024, with projections suggesting it could reach 10% in the final reading of the year. Lula da Silva’s administration has significantly increased public spending, eroding investor confidence in the sustainability of the country’s finances. Additionally, the Central Bank of Brazil has diverged from its regional counterparts by raising its benchmark interest rate to 12.25% in a bid to combat inflation, which has climbed above 4%. This has led to a rise in public sector interest payment expenditures.

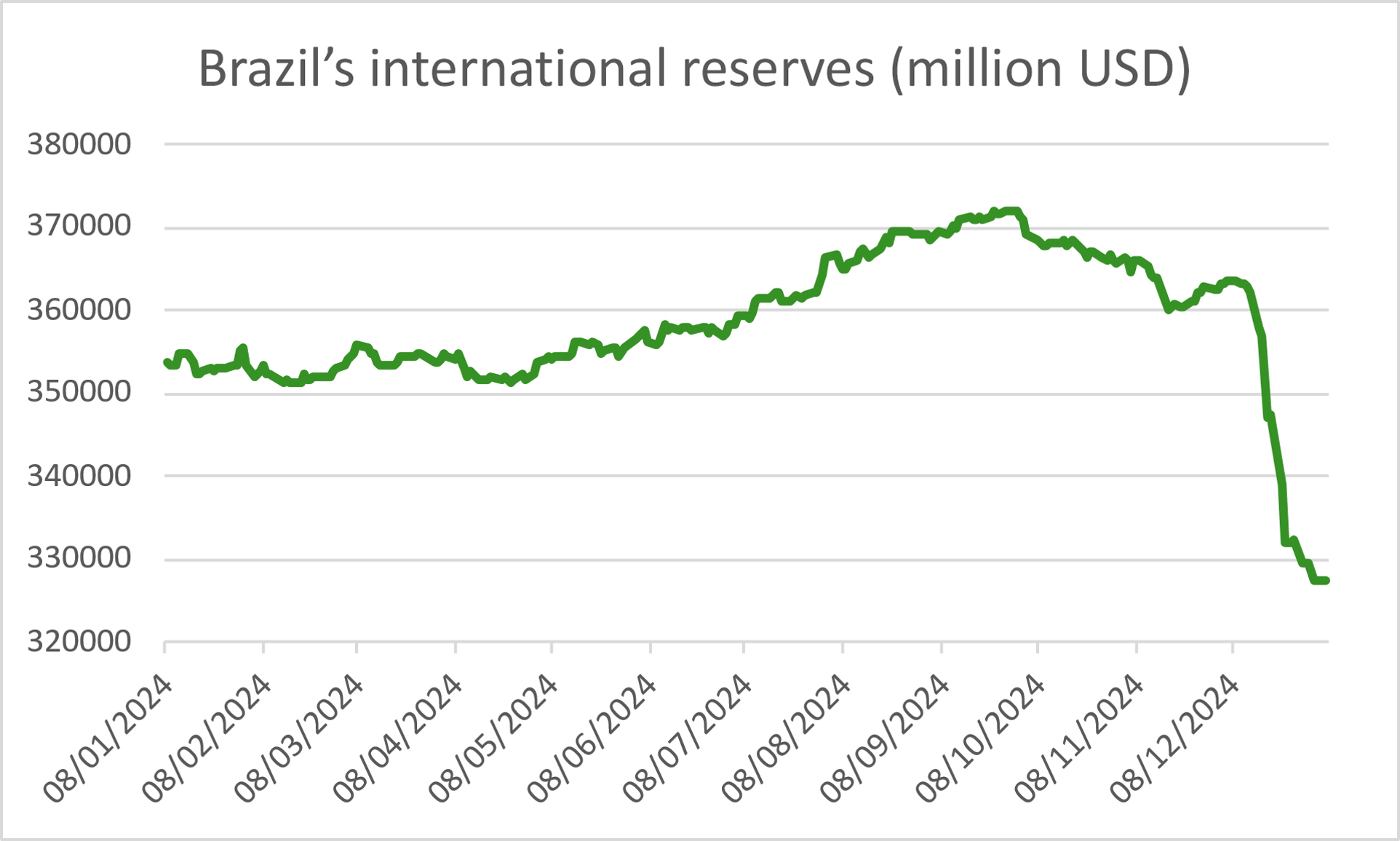

To prop up the real, the Central Bank has intervened in the market, selling USD 50 billion worth of international reserves in recent months. We believe that this is merely a temporary fix, providing only a brief respite. With regard to interest rates, even if inflation were to fall, lowering the benchmark rate would make government bonds less attractive. It seems that the only path to restoring some stability—and with it, renewed interest in Brazilian assets—is for the government to commit to fiscal discipline, meaning a drastic reduction in public spending. Until we see meaningful process in this direction, and despite valuations that may seem tempting, we prefer to steer clear of Brazilian equities and local currency bonds.

Date of report: January 8th 2025