Bond vigilantes are fixed income market participants who, through their investment decisions, exert pressure on governments to maintain responsible fiscal policies. When these bond vigilantes detect excessive fiscal deficits, mounting public debt or policies that risk fuelling inflation, they respond by selling off government bonds en masse. This leads to a sharp rise in yields, increasing the cost of borrowing for the state and forcing policymakers to reassess their course.

There have been notable instances of this dynamic in action. In the US during the 1990s, under President Bill Clinton, rising budget deficits unsettled the market. The bond vigilantes sold off Treasury bonds, pushing the 10-year yield above 9%. This reaction prompted the Clinton administration to implement spending cuts and tax increases, ultimately bringing the deficit and bond yields back down. Another instance of bond vigilantes occurred during the eurozone debt crisis of 2010–2011, causing yields on Greek and Italian government bonds to soar. Greece was effectively shut out of market financing as its interest costs surged past 30%, necessitating a bailout by the IMF and EU, tied to stringent austerity measures. Italy’s 10-year bond yield surpassed 7%, a level widely seen as unsustainable. This culminated in the resignation of Prime Minister Silvio Berlusconi and the appointment of Mario Monti. More recently, the UK faced its own bond vigilantes moment. In 2022, then-Prime Minister Liz Truss unveiled a budget containing a large package of unfunded tax cuts. The bond vigilantes responded by dumping gilts, causing yields to spike dramatically. The Bank of England was forced to intervene to stabilise the market, and Truss resigned just 45 days into her premiership. In Japan (2023-2024), after decades of ultra-low interest rates, investors began to question the sustainability of that policy, triggering a sell-off in government bonds that pushed yields higher. This prompted the Bank of Japan to ease its yield curve control, allowing for greater rate volatility.

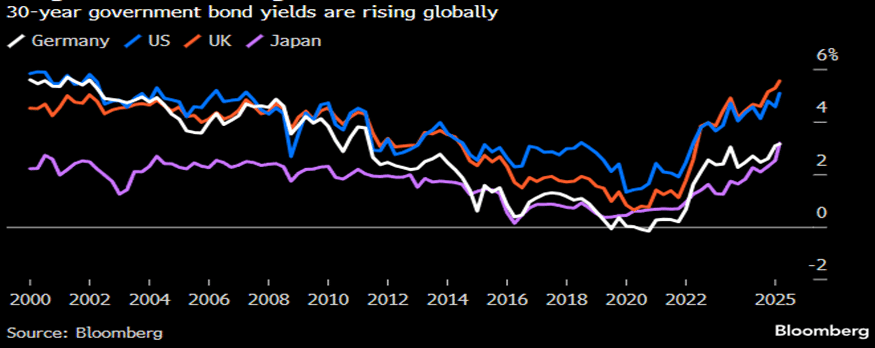

We believe that, geopolitics notwithstanding, fiscal policy and the cost of servicing public debt will be the primary drivers of fixed income markets.Yields have risen across major economies this year as investors grow more sceptical of governments’ ability to finance large budget deficits.

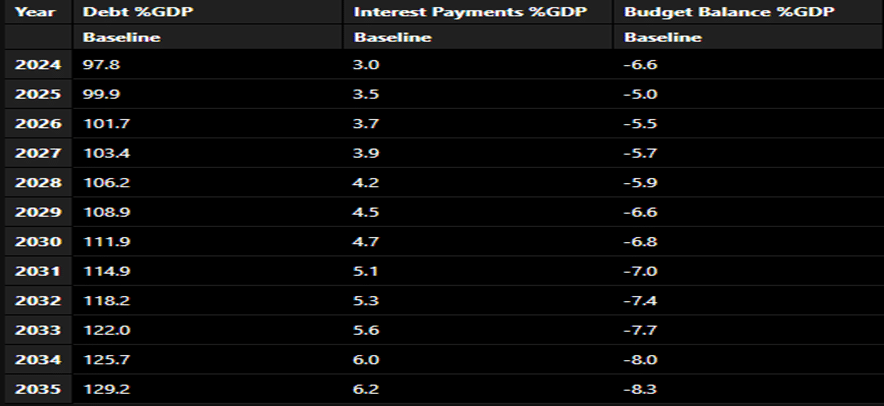

In the second quarter, signs of weaker demand emerged in government bond auctions. In the US, the Treasury sold USD 16 billion in new 20-year bonds. This is a small portion of the USD 514 billion it aims to raise by the end of June. The bonds were sold with a yield of 5.047% and just ahead of the bidding deadline, an indication of lukewarm demand. This marked the highest yield since the maturity was reintroduced in 2020. Compounding matters, Moody’s downgraded the US credit rating from AAA to AA1, aligning it with the other two major agencies. The downgrade cited deteriorating fiscal metrics and the likelihood that persistent, elevated deficits will further increase both public debt and interest burdens. The following table shows US fiscal projections through 2035 (source: Bloomberg).

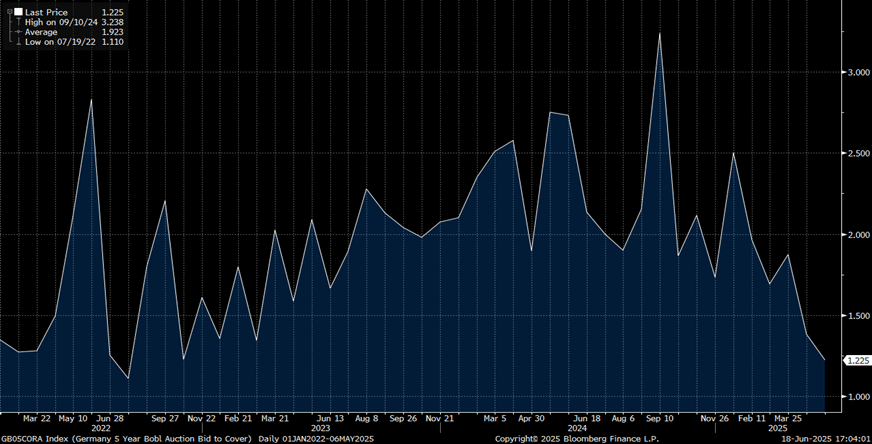

The phenomenon is not limited to the US. For instance, Japan has seen poor take-up in recent bond auctions, with investor appetite waning amid increased global debt market volatility. Germany also experienced soft demand in early June, with bid-to-cover ratios for five-year Bunds falling to 1.225x, the lowest since 2022. Below is a chart showing the bid-to-cover ratio trend for the 5-year German Bund.

The term “bond vigilantes” doesn’t refer to specific individuals, but rather the market’s collective ability to discipline governments it deems fiscally reckless. They do so by selling bonds, pushing yields higher, increasing financing costs and ultimately forcing political course corrections. With central banks now winding down their balance sheets, it will fall to investors to absorb the substantial volumes of sovereign debt expected to fund defence, infrastructure, and other public investment initiatives. Should this spending fail to generate sufficient growth, questions around debt sustainability could resurface. This would revive the bond vigilantes, who may demand higher returns, especially on the long end of the yield curve.

Date of report: June 23rd 2025