What can we expect from fixed income markets in 2025?

Fixed income assets enjoyed a good year in 2024. The main drivers were the interest rate cuts by most central banks and a compression in credit spreads. In the Eurozone, this has translated into a 2% return on the government bond index, 4.75% on the corporate bond index and 8% in the high yield segment. As we enter the new year, the question is: what can we expect?

While there is broad consensus on the resilience of the global economy, downside risks persist, including the impact of geopolitical conflicts, escalating trade tensions under the new Trump administration, and concerns about rising public debt in the major economies. As a result, it appears likely we will see greater volatility, especially after the interest rate volatility index (MOVE) hit its lowest level of the year in December.

Central banks are expected to continue cutting rates in 2025, but this is unlikely to be as coordinated as the rate hikes were. Instead, each economic area will focus on finding its own neutral rate. It is widely anticipated that the ECB will cut rates by 25 bp at every meeting until mid-year, potentially bringing its deposit rate below 2% (of course, this will depend on how inflation risks materialise and the impact of a sharp depreciation of the euro). The Federal Reserve, on the other hand, is likely to move more cautiously, potentially skipping rate cuts at some of its upcoming meetings, aiming for an initial target of around 2.75-4% for its benchmark rate.

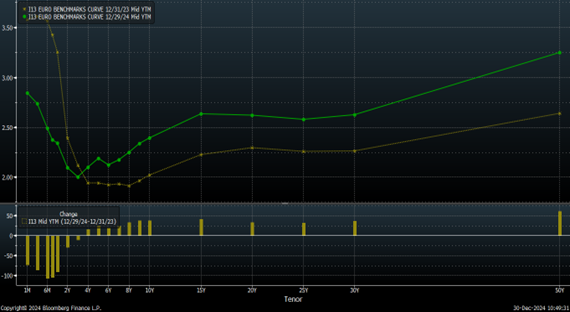

In 2024, the term structure of interest rates (TSIR) on the Eurozone yield curve recorded a decline in short-term rates (-100 bp for the 6-month to 1-year segment), an increase of +40 bp for the medium-to-long segment, and a +60 bp rise in the ultra-long segment.

In 2025, we expect a steeper curve, providing a more attractive term premium for investing in longer maturities. On a technical level, there is also concern about the ECB’s balance sheet reduction, as it will involve purchasing fewer bonds. This means investors will need to absorb this additional supply, potentially demanding higher yields to compensate for the increased volume of issuances (in such a case, particular caution should be exercised with investments in long duration bonds). We will likely shift our focus from monetary policy to fiscal policy, with national deficits coming under scrutiny (particularly in France). We will also be looking at the February elections in Germany, which could determine whether there is room to raise the spending ceiling or introduce any form of joint EU issuance, for instance, in the defence sector.

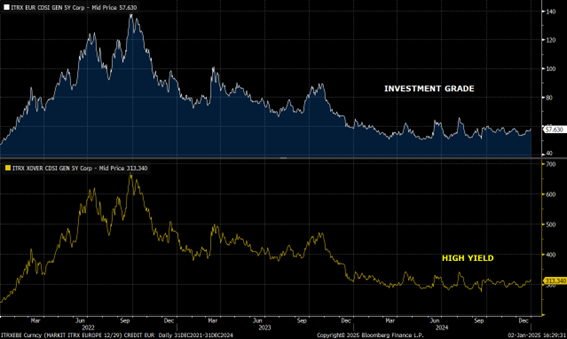

Private fixed income remains well-supported despite the rally in 2024. It offers value compared to the swap and government bond curves, with still-attractive yields providing a carry that acts as a buffer against potential adverse market movements. If 2024 was a story of credit spread compression, current levels now appear demanding. As central banks approach their terminal rates, future levels will increasingly be determined by growth data and the specific fundamentals of issuers. With this in mind, we would not rule out some widening in the spreads, given the current levels.

In terms of fundamentals, the financial sector stands out for its well-managed credit risks, with a stable risk cost and low default rates. Additionally, institutions are showing strong capital and liquidity profiles, with Italian and Spanish banks, in particular, reporting significant gains. For corporate issuers, credit fundamentals remain solid, with improvements in liquidity and leverage ratios in their long-term average. EBITDA margins are also expected to improve, driven by anticipated cost reductions. Major credit rating agencies are reporting more upgrades than downgrades, and default expectations remain at low levels.

Date of report: January 8th 2025