“The economy, stupid” was a popular slogan used in Bill Clinton’s 1992 US presidential campaign that ultimately took him to the White House. If we paraphrase it and replace “economy” with “politics”, we can largely explain the evolution of government bond yields.

Let’s see some examples. The yield of the Gilt (the UK government bond) rose sharply from 1.8%, where it was trading on 1 August 2022, to 4.5% on 27 September that same year, due to the proposal by the government of the new Prime Minister Liz Truss to cut taxes and at the same time increase spending on energy subsidies. Investors feared that this could put the government’s finances on an unsustainable trajectory. The result: the Bank of England was forced to intervene to stabilise the Gilt and, some 44 days later, Liz Truss announced her resignation after withdrawing the plan.

More recently, French President Emmanuel Macron, after analysing the results of the last European elections, called legislative elections in France. The political uncertainty has meant increased scrutiny of the country’s finances which now show debt and deficit dynamics that are worse in many respects than peripheral countries. Early polls had Marine Le Pen’s party (RN) as the clear winners, and investors feared greater fiscal impulse, pushing the risk premium (10-year yield spread between the French and German government bonds) to above 80 bp, equalling the highs of 2017. After the first results, which allowed for a certain status quo and less ambition in terms of fiscal policy measures, the risk premium fell gradually.

As we know, this is a year of many elections. For instance, in the UK, where the Labour Party will govern with a significant majority and, for the time being, the financial markets do not appear too concerned, since opinion polls had been predicting this result for weeks, November will see elections in the US (with a new Trump presidency predictably leading to higher deficits and debt). And there will be elections next year in Germany, where the far-right AfD is considering a referendum on DEXIT. They are moments that can lead to greater volatility in government bond yields.

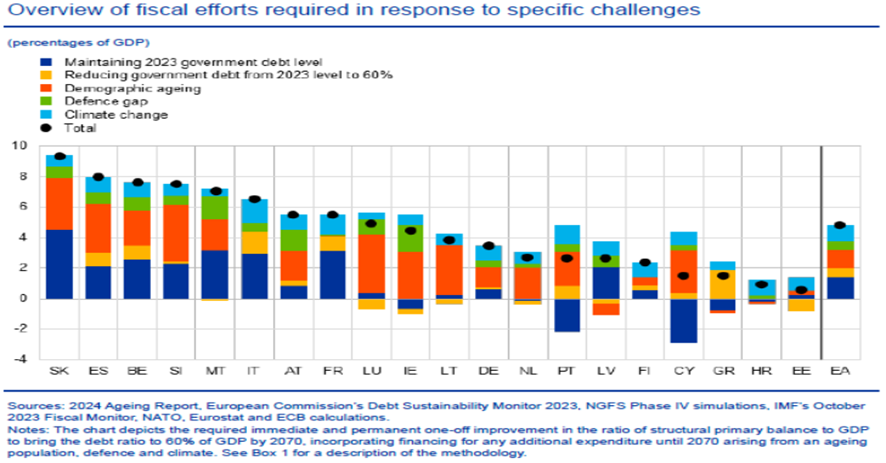

The ECB also takes a view on debt developments and warns of the huge long-term fiscal risks stemming from the ageing population, defence spending and climate change, indicating that the fiscal efforts needed to respond to these specific challenges could amount to at least 5% of GDP.

While borrowing needs are high, sovereign financing conditions have improved. There continue to be beneficiaries of higher demand, as investors seek to capture higher returns before the expected cuts by the central banks are implemented. In this regard, we can summarise the messages from the Sintra Forum (ECB forum that brings together central bank governors, academics and financial sector representatives to discuss monetary policy). Although the market is discounting up to two rate cuts from the Federal Reserve before the end of the year, the Fed is in no hurry to cut back as it awaits more evidence on disinflation and is keeping an eye on the labour market. The ECB, for its part, points to one or two additional cuts this year with the focus on wage developments.

Date of report: July 10th 2024