Monetary easing is the main catalyst for fixed income

Fixed income assets performed well during the year with the primary catalyst being the lowering of interest rates by most central banks. The Bloomberg Euro-Aggregate: Treasury government bond index has posted a return of +1.97% through the third quarter, while the corporate fixed income index Bloomberg Euro-Aggregate: Corporates has returned +3.83% in the first three quarters of the year.

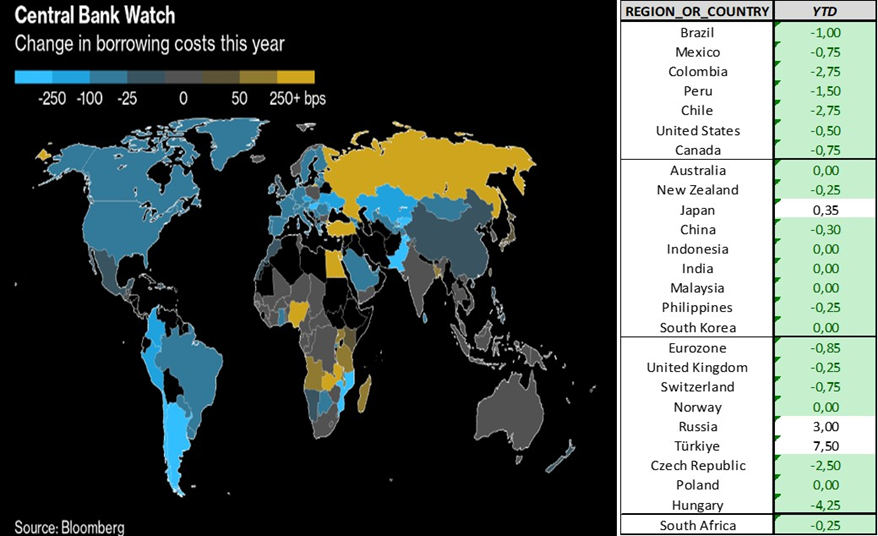

The new mantra of central banks is “there is no set path”, “it will depend on the data” and “decisions will be made meeting by meeting”. With inflation moving towards the 2% target, the easing cycle continues and future rate cuts are expected in upcoming meetings. In fact, investors are pricing in a terminal rate at the end of next year of 1.75% by the ECB (-1.75% over the deposit facility rate of 3.5%) and 3% by the Fed (-2% over the benchmark discount rate which currently stands at 5%). It is likely that not all of the cuts that are being discounted so quickly will be delivered, although ultimately it will all depend on the evolution of inflation and growth, with a particular focus on the labour market.

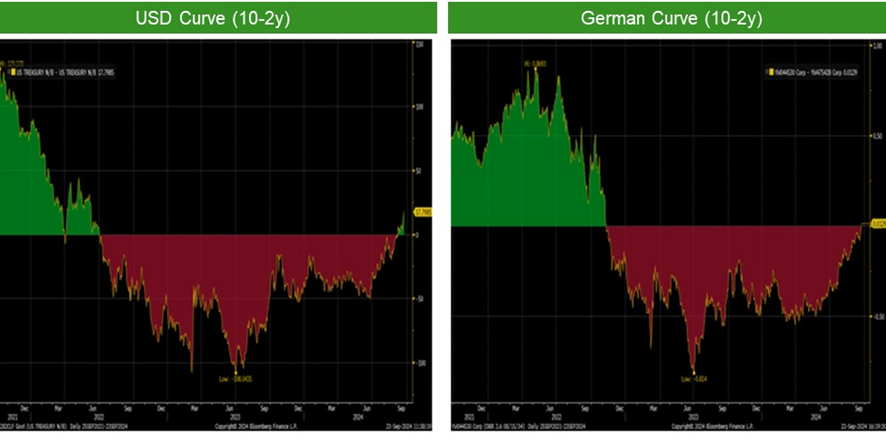

Concerns about a weak economy and its role as a safe haven due to geopolitical factors and increasing nervousness surrounding the US elections have pushed bond yields lower (on 30 September, the Bund was at 2.122% and the 10-year Treasury at 3.782%), pushing bond prices higher. Another effect of monetary easing is that it has allowed the 10-2 year spread to normalise. Thus, in the US this spread has risen to +17 bp and in the Eurozone it has turned positive for the first time since December 2022.

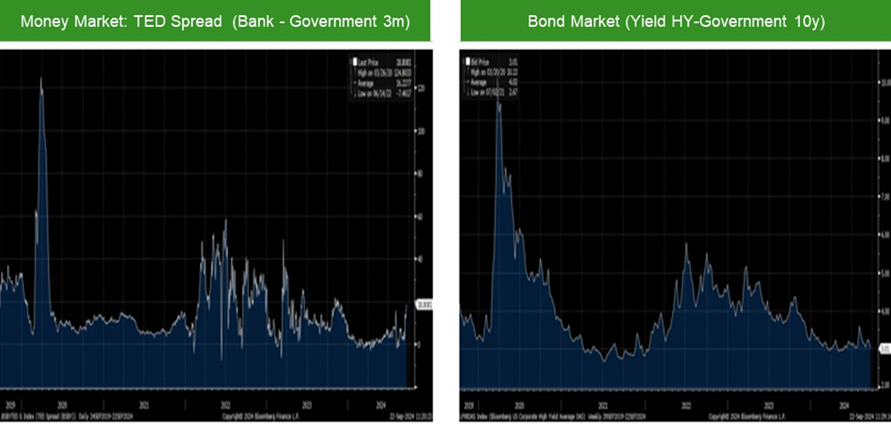

There is still an abundance of liquidity in the market and for now, we are not seeing any signs of strain in financial solvency conditions. There are some indicators illustrating this clearly. For example, in the money market, the TED Spread (difference between interest rates on interbank loans and on the 3-month T-bill) is at a record low. Similarly, in the bond market, the spread between High Yield bond yields and 10-year government bonds is also at a minimum. High Yield bonds have benefited from the surge in risk appetite following interest rate cuts, along with a default rate that hasn’t spiked. The ratings agency Moody’s predicts that the global default will fall further to 4% by the end of the year and then down to 2.8% within 12 months.

If the current market complacency we have mentioned starts to fade, we could see bond yields rise slightly, which would present a good opportunity to enter the market at more attractive levels. After the strong performance of bonds in general throughout the first three quarters of the year, in this final quarter, we prefer to adopt a more cautious approach and focus on tighter risk management. We believe it is more prudent to take a cautious approach when selecting higher-risk assets, in case the anticipated rate cuts do not offset the growing geopolitical risks and the weaker economic data being released.

Date of report: October 7th 2024