When we talk about elasticity in microeconomics, we’re not referring to the ability to do the splits in a Pilates class. No. In this context, elasticity refers to how much one variable (for example, the quantity demanded of a good) changes when something else changes—such as its price, the consumer’s income or the price of a related product. In other words, it is a measure of the sensitivity—sometimes the hypersensitivity—of economic agents to certain stimuli.

The best-known form is price elasticity of demand. This marvellous metric tells us how much the quantity demanded of a good changes when its price changes. If the price of potatoes rises and people stop buying them as if they’d gone off, we’d say that the price is elastic. On the other hand, if the price goes up and people keep buying them as usual, demand is inelastic.

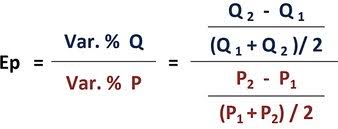

So, how is this economic gem calculated? Easy. There’s a formula:

If the result is greater than 1, demand is elastic (i.e., it changes significantly). If it is less than 1, it is inelastic (it changes little). If the result equals 1, we’re dealing with unit elastic demand—not terribly exciting, but economists like to mention it so it doesn’t feel left out.

Why does this matter? Because it directly affects revenue. If you sell a product with inelastic demand (like petrol), you can raise the price and earn more. However, if you are selling ice cream on the beach and get carried away with your pricing, you might end up with a mess of melted cones and no sales.

Price elasticity of demand isn’t the only type, of course. Price elasticity of supply measures how producers respond to price changes. If prices rise and producers ramp up production, supply is elastic. If they barely react, supply is inelastic. There’s also income elasticity of demand, which tells us how demand shifts when income changes. If you earn more and start buying more sushi, it’s a normal good with positive elasticity. If you earn more and stop buying instant noodles, it’s an inferior good (and your taste buds thank you).

Then there’s cross-price elasticity, which looks at how the demand for one good changes when the price of another changes. If coffee prices rise and tea demand goes up, the two goods are substitutes. If printer prices rise and cartridge demand falls, they are complementary goods. If nothing changes at all, perhaps the goods are unrelated—or the consumer is just confused.

A note for the curious: elasticity is a useful tool, but it stems from human behaviour, which is what really matters. Individual choice—subjective and contextual—is the true driving force. Elasticity offers insights, but it never replaces the judgement of players in the market. And although it might seem like pure mathematics, at its core, it’s about decisions, desires and priorities. Ultimately, it’s about us.

Here’s an example. Imagine the price of bread goes up. Conventional theory says that if demand falls sharply, it’s elastic. But with a critical lens, we should ask: Why, exactly, are people buying less bread? Have preferences changed? Have people switched to a gluten-free diet? Are they worried about inflation? Did a viral TikTok recommend intermittent fasting? Elasticity tells us the “what”, but not the “why”. And it’s the “why” that really matters if we want to understand economics as the science of human action. Elasticity doesn’t act, it doesn’t choose, it doesn’t dream of beach holidays. People do. So yes, elasticity is useful—but handle it with care. It’s not the Oracle of Delphi. It’s more like a torch, shining light on part of the path.

Diari d’Andorra 14.05.2025